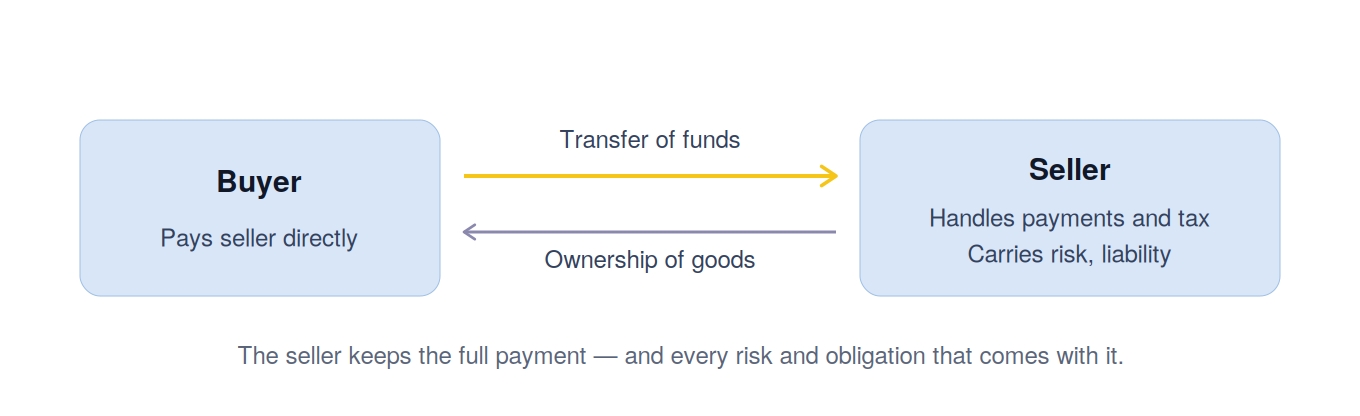

Building a B2B marketplace offers massive growth opportunities, but it also means managing multi-vendor payouts, cross-border VAT, and corporate payment terms- all of which can introduce severe operational complexity. To win over business buyers, offering flexible net terms is no longer optional. The core challenge for operators lies in managing the underlying credit risk of the net terms without overwhelming internal finance operations.

When structuring a digital platform, operators typically weigh two approaches: outsourcing the transaction to a Merchant of Record (MoR) or implementing a dedicated B2B Buy Now, Pay Later (BNPL) infrastructure. Below, we look at how each works, where they differ and which scales better.

What is a Merchant of Record (MoR)?

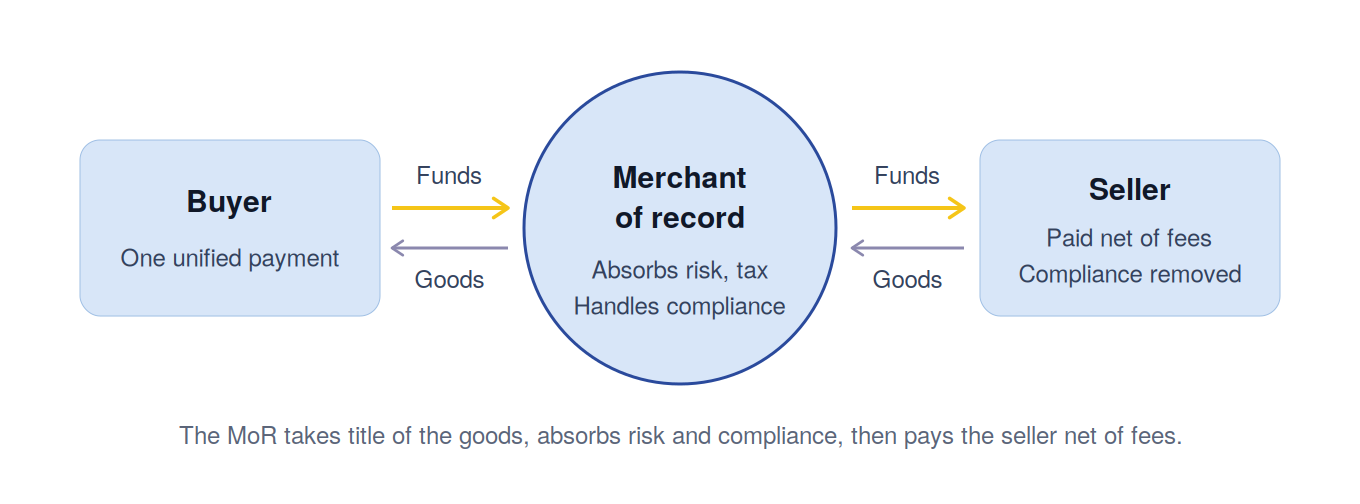

A Merchant of Record (MoR) is the legal entity responsible for processing customer payments, handling chargeback disputes, and ensuring cross-border tax compliance, such as VAT or GST.

In practice, MoR acts as a reseller: it purchases the goods from the vendor and sells them to the end customer. For a marketplace, this removes the administrative burden of registering for tax in every country where buyers sit, the MoR carries that compliance.

The upside? Speed. Instead of spending months adapting to localized tax laws, the platform can start selling in new markets right away because the local payment methods are already in place, and the MoR takes care of KYC, Anti-Money Laundering (AML), and fraud checks.

Where the MoR model falls short

Although the MoR model removes real administrative burden, it comes with trade-offs that grow more expensive as a marketplace scales:

- Fees scale with revenue: MoR pricing typically runs 5–8% of the full transaction value. This margin-eating percentage stays constant no matter how large your platform grows.

- Limited flexibility and control: MoR platforms are largely one-size-fits-all, with little support for customized enterprise contracts or varied commercial terms. Subsequently, you give up control of critical aspects of your business, including customer data, customer service touch-points, and refunds.

- Payout delays: MoRs may hold funds longer for regulatory requirements or manage their own cash flow, leaving your vendors waiting for payouts.

- Net terms aren't solved: An MoR's role covers payments, tax, and chargebacks. Underwriting business buyers and carrying the credit risk of 30-, 60- or 90-day terms sit entirely outside of their scope. Hence, the marketplace still needs a separate answer for trade credit.

The Modern Alternative: Pure B2B BNPL

BNPL B2B takes the opposite approach: instead of restructuring who legally sells the goods, it solves the financing problem directly at checkout.

Vendors remain the sellers of record and keep their customer relationships, while the BNPL provider underwrites the buyer, pays out upfront, and absorbs the credit risk. The compliance, invoicing, and payout complexity is handled around the transaction rather than by rerouting the transaction itself.

This is the model Two is built on. Two handles the underwriting, compliance, and payout-routing demands of global B2B marketplaces. Here is what that looks like in practice:

- Instant approvals. Delphi, Two's AI credit engine, approves legitimate businesses at checkout in under two seconds, eliminating PDF forms, long wait times, and abandoned carts.

- Higher credit limits. Two offers up to 7x higher limits than traditional credit bureaus, giving buyers more purchasing power and lifting average order value (AOV).

- Automated split payments. When a buyer checks out with multiple vendors in a single cart,Two pays each vendor instantly upon fulfillment while sending the buyer one consolidated invoice.

- Full credit and fraud protection. Financing through Two is entirely non-recourse: backed by Frida, Two's fraud engine, the platform absorbs 100% of credit and fraud risk, so a buyer default never lands on your balance sheet.

- Compliant e-invoicing. Two automatically generates country-specific corporate invoices that meet varying mandates, removing cross-border compliance risk without requiring complex reseller structure.

Merchant of Record vs. B2B BNPL: At a Glance

So, which approach scales?

An MoR solves tax and payment administration by becoming the seller. While that structure suits digital goods with a single seller, it breaks down under multi-vendor marketplace volumes where the MoR must legally contact with and buy from every individual vendor. Even more importantly, it leaves the trade credit problem untouched.

B2B BNPL solves the harder problem: it puts net terms, underwriting, risk transfer, and compliant invoicing at the point of sale, while vendors keep their sales and the platform keeps its margin. For a marketplace whose growth depends on offering net terms safely, B2B BNPL is the approach that scales.

👉 Building a global B2B marketplace? Talk to our Marketplace Experts

FAQ

What is a Merchant of Record (MoR)?

An MoR is a legal entity that processes customer payments and handles cross-border tax compliance, fraud, and chargebacks. It acts as a reseller, technically buying goods from the vendor and selling them to the end buyer to offload the platform's administrative burdens.

How does B2B BNPL differ from an MoR?

An MoR focuses on global tax compliance and legal payment processing by acting as an intermediary. In contrast, B2B BNPL is a financing infrastructure that integrates into the checkout to manage real-time credit underwriting, default risk, and net payment terms.

How does B2B BNPL handle multi-vendor orders?

It uses automated split-payments. When a buyer purchases from multiple vendors at once, the system sends a single, consolidated invoice to the buyer while automatically routing individual, immediate payouts to each vendor upon fulfillment.

Who bears the risk if a buyer defaults?

With a modern B2B BNPL solution, the financing is non-recourse. The BNPL provider's risk engine underwrites the buyer at checkout and absorbs 100% of the credit and fraud risk, completely protecting the marketplace's balance sheet.

Why is instant credit underwriting necessary for marketplaces?

Traditional trade credit relies on manual, multi-day checks that contribute to cart abandonment and procurement friction. Automated real-time underwriting approves corporate buyers at checkout in seconds, keeping conversion high and lifting average order values.

Can a marketplace use both an MoR and B2B BNPL?

Yes. The two solve different problems, so they aren't mutually exclusive. However, since a modern B2B BNPL provider also handles compliant invoicing, payout routing, and risk, many marketplaces find that BNPL infrastructure alone covers their needs without the cost and control trade-offs of a reseller structure.